Financial Sustainability: Lender Appetite for the Higher Education Sector

Financial Sustainability: Lender Appetite for the Higher Education Sector

Major banks have typically been the main providers of short-term facilities to the Higher Education (“HE”) sector, with these facilities ranging from two to five-year tenors (and occasionally longer for the highest quality HEIs), with possible options to extend at lender discretion. For longer term borrowing, the sector has looked to institutional finance from capital markets in the form of listed bonds or private placements, which have provided up to 50+ year tenors. Due to increasing underlying funding costs, since late 2021 there has been very little long-term borrowing sought by universities from institutional funders. Instead, universities in need of further liquidity have focused on overdrafts or revolving credit facilities (“RCFs”).

Historically, many universities have held RCFs to provide an additional liquidity buffer, or in certain cases, to fund capital expenditure. Where used as a liquidity buffer, these facilities have often been undrawn. The HE sector continues to face challenges with pressure on operating surpluses and cash reserves due to rising cost bases, frozen tuition fees and volatility in international student recruitment. Over the past 12 months, we have seen a rise in universities seeking additional working capital facilities to help mitigate cashflow timing issues, provide a buffer for downside scenarios or finance investment with the aim of refinancing to longer term facilities if longer term borrowing rates decline.

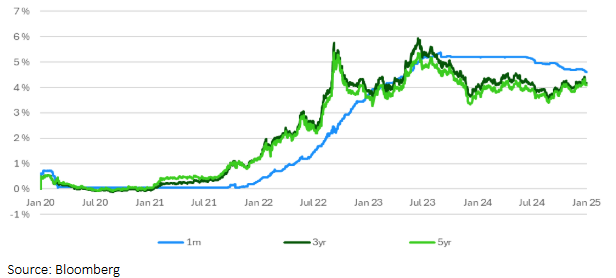

Despite the headwinds, pricing for short-term facilities for the sector remains favourable, although we are starting to see a wider divergence in funding terms between lenders. Some lenders are pricing competitively to secure new business or opportunistically grow their loan book whilst others are doing the reverse to shrink their exposure to the market. Also, lenders are increasingly requiring more due diligence, scrutiny of forecasts and strategic plans to obtain credit approval for new facilities. RCFs are typically priced as a margin over SONIA (Sterling Overnight Interbank Average), which is a backward-looking rate, based on actual transactions. It reflects the average of the interest that banks pay to borrow sterling overnight from other financial institutions and institutional investors. Current (as at Jan 25) 1-month SONIA is c. 4.6%, with 3- and 5-year SONIA swaps reducing to c. 4.1%-4.2%. Margins over SONIA can range on average between 0.4%-1.50% depending on the perceived credit quality of an institution – though HEIs at the perceived top and bottom of the sector might see improved or less favourable terms. Pricing is typically lower for shorter tenors and can often be improved when additional services are obtained with a lender (i.e. transactional banking).

Historical SONIA Swaps January 2020-25

Lenders with more exposure to the sector are increasingly only considering facilities for existing customers, and in limited instances have declined to provide terms for these customers. Lender appetite for the sector is polarised by ranking and perceived credit quality. Bank term loans or RCFs in recent years have been limited to 3 -5 year tenors. However, we are starting to see Russell Group institutions and other well ranked institutions that can demonstrate strong cash flow generation being offered terms up to 7 years and obtaining competitive terms from multiple lenders. Smaller, or mid and lower ranked, institutions are facing increasing due diligence and relying on their existing lenders for new liquidity, due to the reduced competition in the market.

When conducting due diligence, banks are typically interested in the following key areas:

- Forecasts – understanding the university’s current forecasts, assumptions, any scenario analysis and how these align with the university’s strategic plans.

- Student recruitment – this will largely depend on where you are in the recruitment cycle, but banks are increasingly looking for the latest application data and comparing this to historical trends at a comparable point in previous cycles, with a particular focus on international recruitment. For international students, banks are often interested in the diversity of students and understanding any reliance on single countries.

- Potential levers – Banks will want to understand levers that the university has already implemented to improve operating surpluses, such as cost savings, capital spend reductions, staff redundancy schemes etc. These schemes often take time to implement and as such, banks are increasingly looking for data on the deliverability of additional savings which have been layered into forecasts in addition to other potential levers that could be pulled in a downside scenario.

- Management – Banks will be keen to meet senior management and where future savings plans are forecast, understand the buy-in from management and governance. They will also want to ensure that management has fully considered the implications of any measures implemented on operating performance.

- Treasury policy – understanding the university’s policies on liquidity, deposits etc.

- Potential draw down profile – while this is not fixed, banks are looking to understand the likely utilisation of a facility. This can help with pricing to balance the non-utilisation fee and interest margin.

How can QMPF assist?

We can provide support to universities looking to manage or review their borrowing.

- Debt options appraisal – Analyse the borrowing options available and suitability for your institution, including working capital facilities, term loans, private placements or income strip funding.

- Refinancing & arrangement of new facilities – We are currently active with a number of clients, supporting them with a review of debt options, covenant negotiations, repayment of existing borrowing (incl. benchmarking of any early termination gain / cost using Bloomberg to access live market data) and procurement of new facilities. Our market coverage means that we can provide you with visibility of the full range of financing options.

- Liquidity and treasury management – As part of this process, you may choose to refresh your wider treasury management policy or benchmark your approach to liquidity. We are retained by several clients to provide ongoing strategic and treasury management advice; leveraging innovation and technology where possible to allow HEIs to make better, more informed strategic decisions.

- Understanding the market and lender engagement – The core of QMPF’s activity lies in Higher Education, having worked with numerous HEIs and supported the sector for over 20 years. We have strong relationships with across the funding market and are in regular contact as part of our wider market engagement. These relationships allow us to have candid discussions with key funder contacts during the process and we find that this approach delivers the best outcome for our clients. We believe that a skilled intermediary can help find solutions and reduce the workload of internal finance teams.

More News…

Contacts